In the previous article we discussed that with compound interest was not very difficult to arrive at a figure of, say, € 300,000.

Well, needless to say, despite not be complicated requiring high doses of patience and discipline. Highly difficult thing when you have a considerable amount of money in hand, the temptation to eat uncontrollably or buying a luxury item, see a car, a house etc. exponentially increase.

A major plus point is the age at which you start, it is clear that the longer devote the most amount of compound interest can gather during a given period of time. So begin no later than age 30 would be ideal.

The first is to score a goal. Then decide how we figure that we will be around for a few years head.

Suppose

we do not want risks and we're moving from, for example, 3-4% will give

us a bank deposit and give us 5-7% by acquiring quality corporate debt. We mark a savings rate X which in monthly maturities of our investments go humble adding interest.

At the end of each year will add to the annual CPI rate of savings we had last year so we make sure we do not lose purchasing power over the years and inflation were not gaining ground.

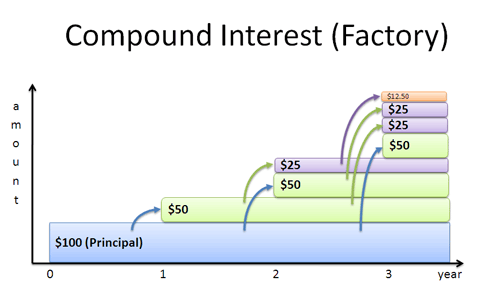

An example. Monthly savings rate € 500, in a year together € 6,000. The next year we will have € 6,000 in an investment for example at 4.5% APR so that at the end of the second year we will have € 6,000 the first year, plus interest of € 6000 to 4.5% (213 euros after tax ( 21%)), but the 6000 euros (plus CPI should have risen to the saving rate) in the second year. A total of 12,213 euros in two years just.

Do you get the idea right? The

third year we invested 12,213 euros, for example, the 4.5% that we will

generate € 434 after tax, but the 6000 (plus annual CPI) for the third

year, in total € 18,647.

In three years we will have € 18,647 without having updated the saving rate not to complicate the explanation. I think it's pretty clear the concept.

It is clear that more and more savings rate interest we reached the goal faster. But the same does not increase the interest savings. If you double the interest rate at which you are making your money work the result will not bend but is multiplied by 3'5. So imagine that can happen maximizing the savings rate and get a higher annual interest average. Spectacular.

It happens snowball effect, the principle is much start but once we have run for anyone.

To give more examples and see how it affects a slight increase projected interest rate over time.

Starting with 0 and with a savings rate of 610 € monthly, 3% compound interest

capitalized through in 20 years we will have about 200,000 euros, in

fact rather more in the calculation because we have not updated the CPI savings rate.

Just changing the 3% to 5% and we almost € 250,000. Can we imagine if we get over it?

If for whatever reason we can start from a number other than 0 that we have gained in time.

Let everyone do their calculations, charts and projections and let your imagination run wild. On the net there are plenty of calculators and compound interest tables .

Anyone is more motivated? You just have to want it.